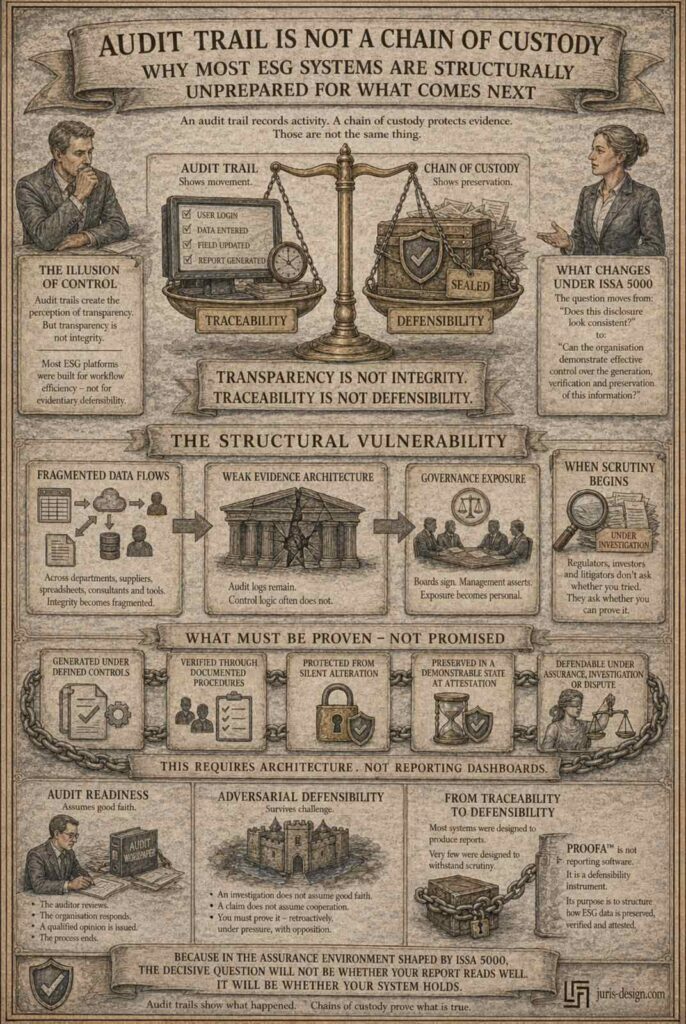

Board Liability in the Age of ESG Assurance

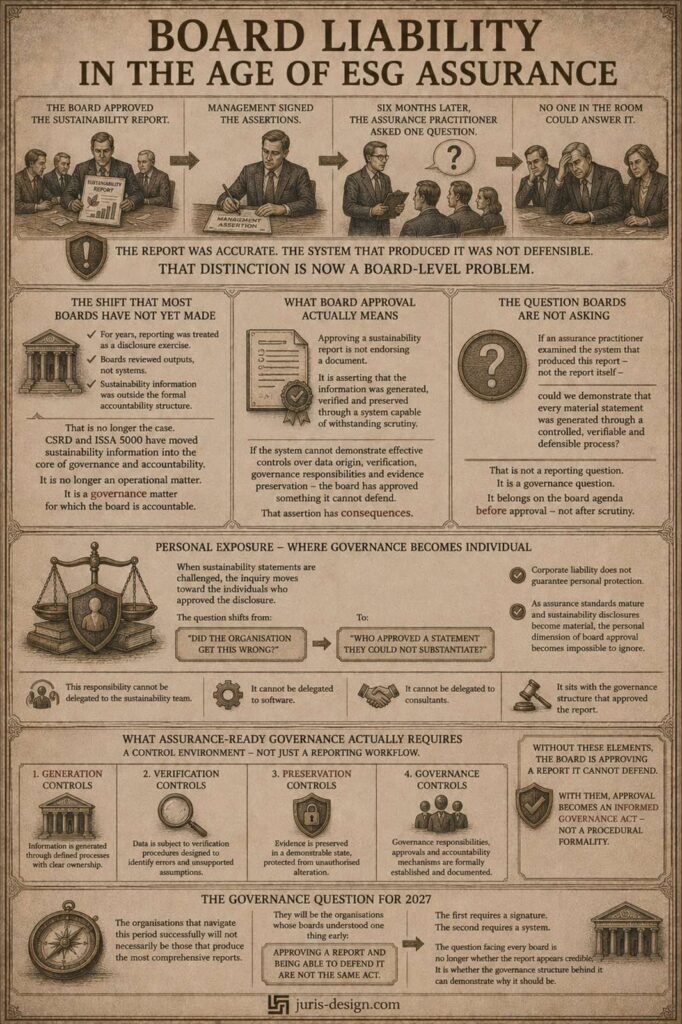

The board approved the sustainability report.

Management signed the assertions.

Six months later, the assurance practitioner asked one question.

No one in the room could answer it.

The report was accurate.

The system that produced it was not defensible.

That distinction is now a board-level problem.

The Shift That Most Boards Have Not Yet Made

For years, sustainability reporting was treated as a disclosure exercise.

Collect the data. Prepare the report. Meet the deadline.

Boards reviewed outputs.

They rarely examined the systems that produced them.

That approach was manageable when assurance expectations were limited and sustainability information existed outside the formal accountability structure of the organisation.

That is no longer the case.

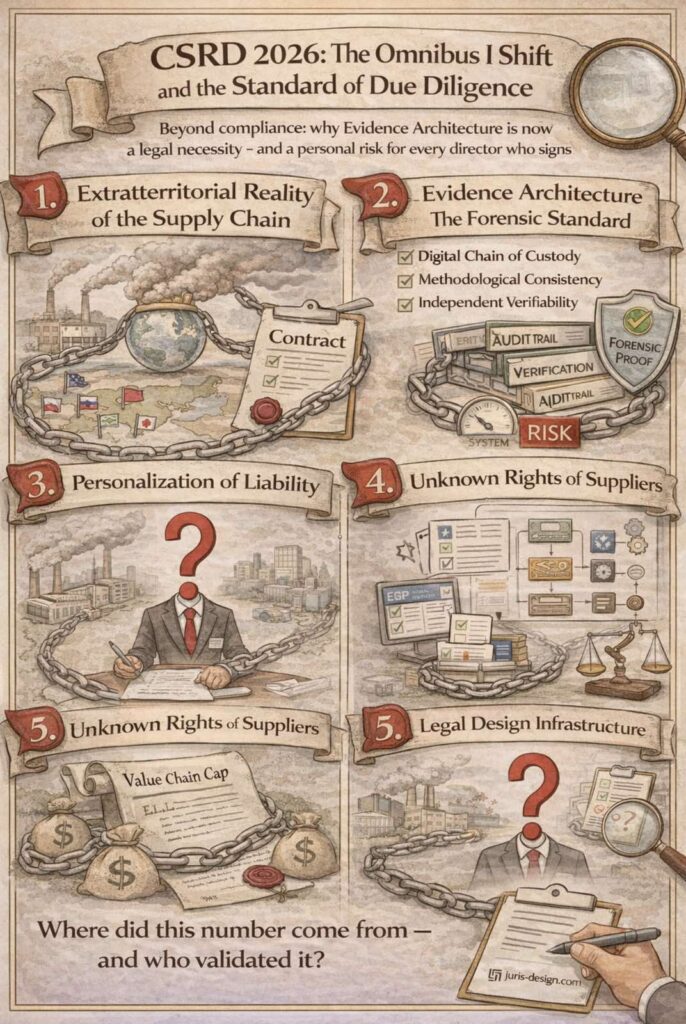

As the Corporate Sustainability Reporting Directive embeds sustainability information into formal corporate reporting, and as the International Standard on Sustainability Assurance establishes the reference point for assurance engagements, the position of the board changes fundamentally.

Sustainability information is no longer an operational matter reviewed by a specialist team.

It is a governance matter for which the board is accountable.

What Board Approval Actually Means

Many directors still experience ESG report approval as a procedural step.

Sign here. Move to the next agenda item.

The legal and operational reality is different.

When a board approves a sustainability report, it is not simply endorsing a document.

It is asserting that the information contained in that document was generated, verified and preserved through a system capable of withstanding independent scrutiny.

That assertion has consequences.

If the system behind the report cannot demonstrate effective controls over data origin, verification procedures, governance responsibilities and evidence preservation — the board has approved something it cannot defend.

And under mature assurance frameworks, that gap does not remain invisible for long.

The Question Boards Are Not Asking

Boards regularly discuss regulatory risk.

They discuss reputational risk.

They discuss financial exposure.

They rarely ask the question that matters most in an assurance environment:

If an assurance practitioner examined the system that produced this report — not the report itself — could we demonstrate that every material statement was generated through a controlled, verifiable and defensible process?

That is not a reporting question.

It is a governance question.

And it belongs on the board agenda before the report is approved — not after scrutiny begins.

Personal Exposure — Where Governance Becomes Individual

Board liability in the context of ESG assurance is not abstract.

When a sustainability statement becomes the subject of regulatory scrutiny, investor challenge or litigation, the inquiry does not stop at the level of the legal entity.

It moves toward the individuals who approved the disclosure.

The question shifts from:

“Did the organisation get this wrong?”

to:

“Who approved a statement they could not substantiate?”

Directors who have relied on the assumption that corporate liability shields personal accountability are encountering a different reality.

As assurance standards mature and sustainability disclosures become increasingly material to investment decisions, regulatory compliance and legal exposure — the personal dimension of board approval becomes impossible to ignore.

That responsibility cannot be delegated to the sustainability team.

It cannot be delegated to software.

It cannot be delegated to external consultants.

It sits with the governance structure that approved the report.

What Assurance-Ready Governance Actually Requires

Assurance readiness is not achieved by possessing audit trails and documented workflows.

Those are necessary. They are not sufficient.

A board that is genuinely prepared for the assurance environment must be able to demonstrate that the organisation operates a control environment — not merely a reporting workflow.

That means:

Information is generated through defined processes with clear ownership.

Data is subject to verification procedures designed to identify errors and unsupported assumptions.

Evidence is preserved in a demonstrable state, protected from unauthorised alteration.

Governance responsibilities, approvals and accountability mechanisms are formally established and documented.

Without these elements, the board is approving a report it cannot defend.

With them, approval becomes an informed governance act — not a procedural formality.

The Governance Question for 2027

The organisations that navigate this period successfully will not necessarily be those that produce the most comprehensive sustainability reports.

They will be the organisations whose boards understood one thing early:

Approving a report and being able to defend it are not the same act.

The first requires a signature.

The second requires a system.

As assurance environments continue to mature, the question facing every board is no longer whether the report appears credible.

It is whether the governance structure behind it can demonstrate why it should be.

Other blogs

Board Liability in the Age of ESG Assurance

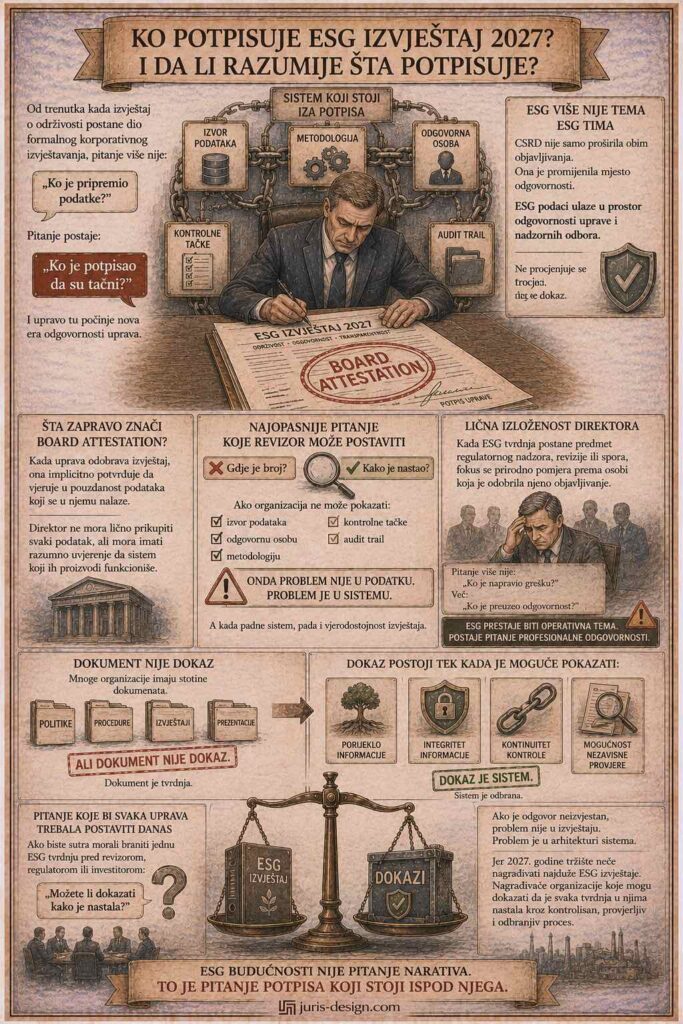

The management board approved the sustainability report. The management signed statements...

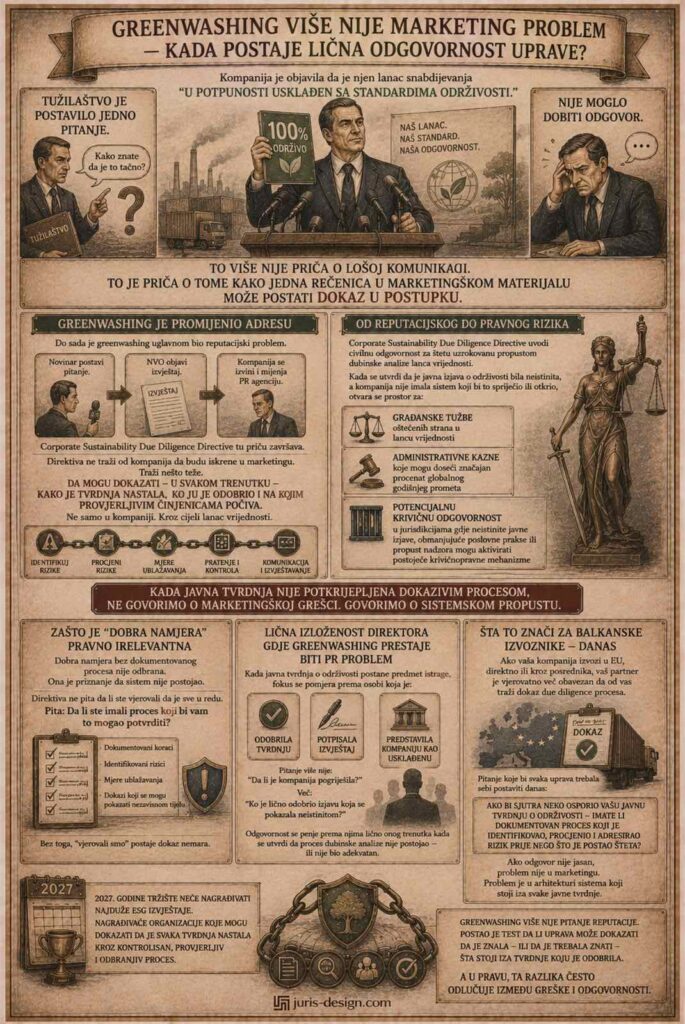

Greenwashing is no longer a marketing problem - when does it become personal liability for management?

The company announced that its supply chain is “fully…