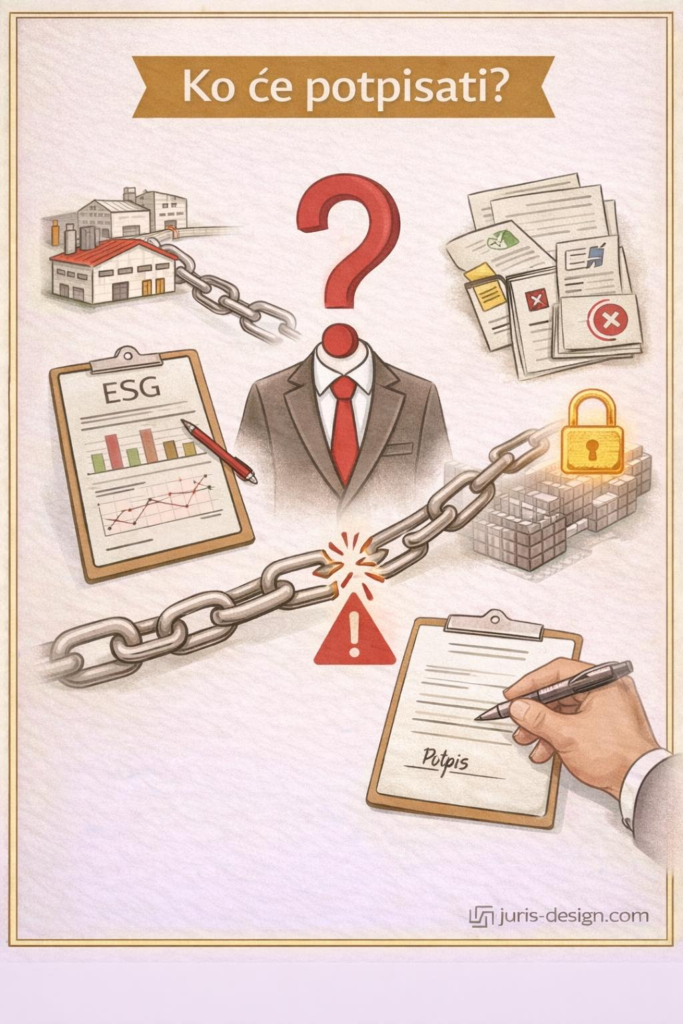

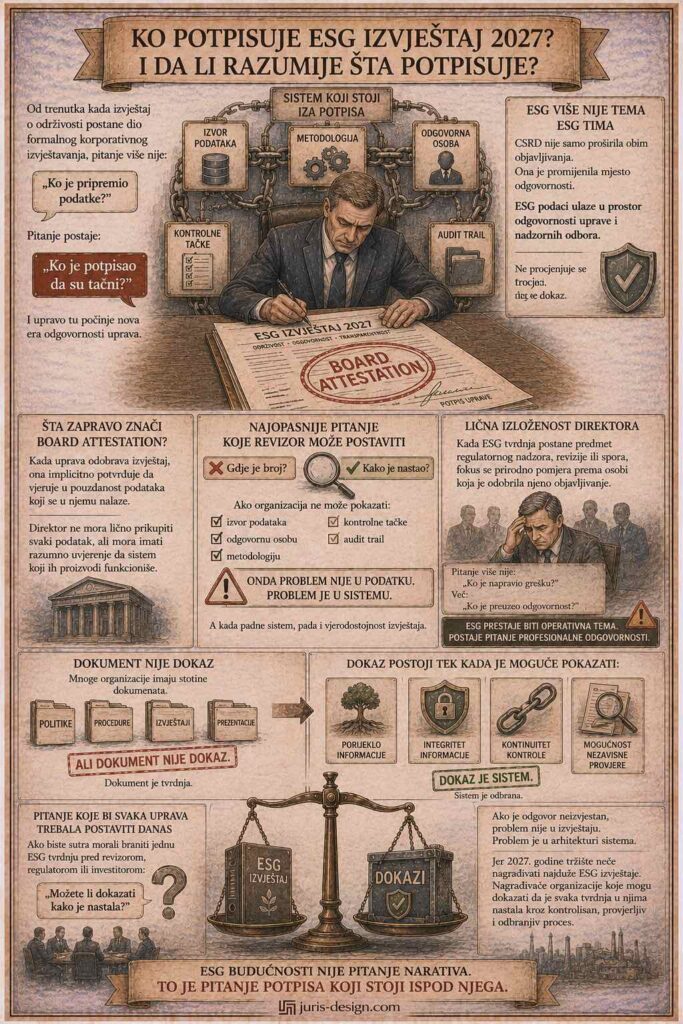

Who Signs the ESG Report in 2027 – and Do They Understand What They Are Signing?

Most companies still view ESG as a compliance project.

That is a dangerous misconception.

Because the moment a sustainability report becomes part of formal corporate reporting, the question is no longer:

“Who prepared the data?”

The question becomes:

“Who signed that it is accurate?”

And that is precisely where the new era of management accountability begins.

ESG Is No Longer an ESG Team Issue

The Corporate Sustainability Reporting Directive (CSRD) did not merely expand the scope of disclosures.

It changed the location of responsibility.

Sustainability is no longer treated as a separate function.

It becomes part of corporate governance.

In other words:

ESG data enters the sphere of responsibility of management boards and supervisory boards.

And entirely different rules apply there.

Effort is not evaluated.

Evidence is.

What Does Board Attestation Actually Mean?

Many directors still perceive an ESG report as a document prepared by the sustainability team.

From a legal perspective, the situation looks different.

When management approves a report, it implicitly confirms that it believes in the reliability of the data contained within it.

That does not mean a director must personally collect every piece of data.

But it does mean they must have reasonable assurance that the system producing it functions properly.

This is exactly why regulatory focus is increasingly shifting from the content of the report to the system that generates it.

The Most Dangerous Question an Auditor Can Ask

There is one question capable of collapsing an entire ESG narrative:

“How do you know this data is accurate?”

Not:

“Where is the number?”

But:

“How was it created?”

If an organization cannot demonstrate:

- the source of the data

- the responsible person

- the methodology

- the control points

- the audit trail

then the problem is not the data.

The problem is the system.

And when the system fails, the credibility of the report fails with it.

Personal Exposure of Directors

Boards frequently discuss regulatory risk.

They discuss personal exposure far less often.

Yet this is where the greatest change is taking place.

When an ESG claim becomes the subject of regulatory scrutiny, an audit, or a dispute, attention naturally shifts to the person who approved its publication.

The question is no longer:

“Who made the mistake?”

But:

“Who assumed responsibility?”

At that moment, ESG ceases to be an operational issue.

It becomes a matter of professional accountability.

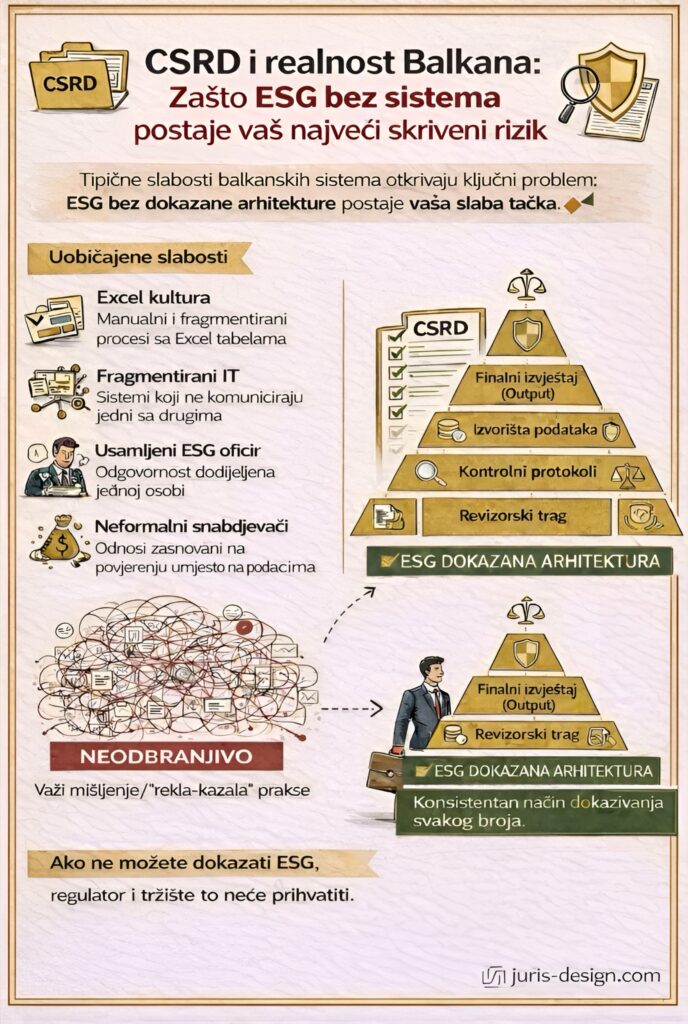

A Document Is Not Evidence

Many organizations have hundreds of ESG documents.

Policies. Procedures. Reports. Presentations.

But a document is not evidence.

Evidence exists only when it is possible to demonstrate:

- the origin of the information

- the integrity of the information

- continuity of control

- the ability to independently verify it

Without that, a document remains only a claim.

The Question Every Board Should Be Asking Today

If tomorrow you had to defend a single ESG claim before an auditor, regulator, or investor:

Could you prove how it was created?

If the answer is uncertain, the problem is not the report.

The problem is the system architecture.

Because in 2027, the market will not reward the longest ESG reports.

It will reward organizations that can demonstrate that every claim within them was created through a controlled, verifiable, and defensible process.

The ESG of the future is not a question of narrative.

It is a question of the signature beneath it.