ISSA 5000 Will Not Test Your ESG Report - It Will Test Your System

For years, sustainability reporting has been evaluated primarily through the lens of disclosure.

Organisations focused on whether required metrics were reported, whether narratives were coherent, and whether sustainability statements aligned with applicable reporting frameworks.

That era is ending.

As assurance expectations mature and the International Standard on Sustainability Assurance (ISSA 5000) becomes the reference point for assurance engagements, the focus is shifting away from what organisations disclose and toward how that information is generated, controlled, validated and preserved.

The distinction may appear subtle.

In practice, it changes everything.

The Traditional ESG Mindset

Most ESG programmes evolved around reporting obligations.

Data was collected from multiple departments, consolidated in spreadsheets or reporting platforms, reviewed by sustainability teams and ultimately transformed into disclosures.

The primary objective was completeness.

Can we gather the information?

Can we prepare the report?

Can we meet the deadline?

In this environment, systems were designed to facilitate reporting workflows.

They were not necessarily designed to create defensible evidence.

As long as disclosures appeared reasonable and assurance expectations remained limited, that distinction often went unnoticed.

ISSA 5000 changes the equation.

The Question Is No Longer About the Report

Historically, organisations have been accustomed to questions such as:

Does the disclosure comply with the framework?

Is the reported information consistent?

Can management explain the methodology?

These questions focus on outputs.

ISSA 5000 introduces a different perspective.

The assurance practitioner must obtain sufficient appropriate evidence regarding sustainability information.

That requirement inevitably shifts attention toward the underlying system.

The real question becomes:

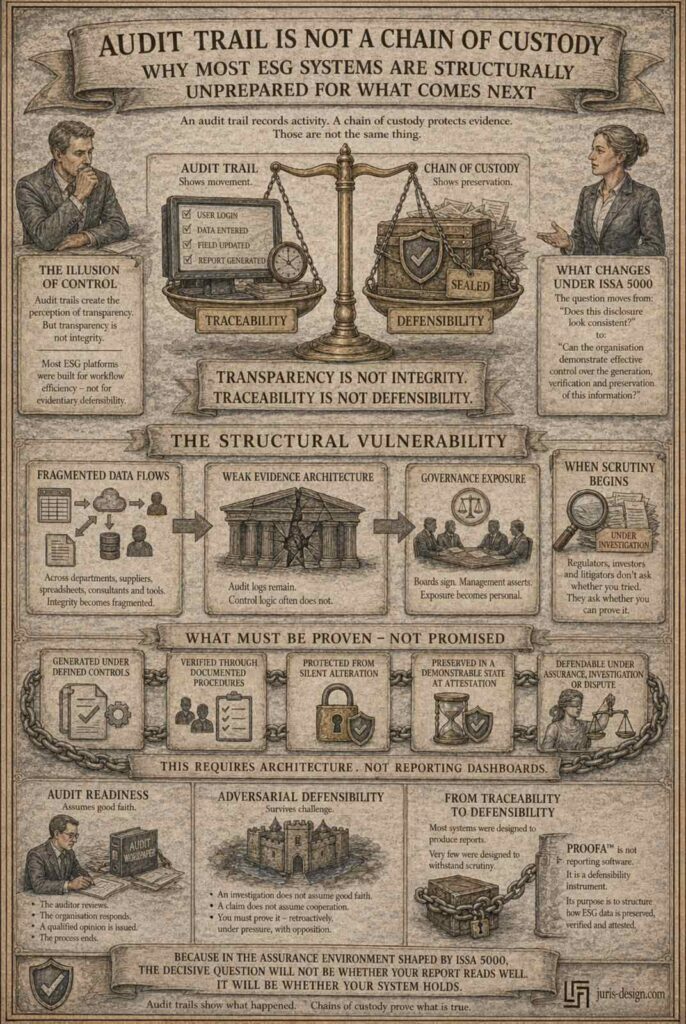

Can the organisation demonstrate effective control over the generation, verification and preservation of sustainability information?

This is not a reporting question.

It is a systems question.

Assurance Begins Long Before the Report

Many organisations still view assurance as a review conducted near the end of the reporting cycle.

That assumption is increasingly problematic.

Evidence quality is determined at the moment information is generated, not when it is reported.

If source data lacks ownership, validation logic, preservation controls or documented procedures, no amount of late-stage review can fully compensate for those weaknesses.

Assurance therefore begins upstream.

It begins with:

- Data origin

- Control design

- Validation procedures

- Governance responsibilities

- Evidence preservation

The report merely reflects the effectiveness of those elements.

Why Architecture Matters

Most ESG systems were built to consolidate disclosures.

Very few were built to preserve evidence.

This distinction becomes critical under assurance.

A reporting platform may successfully aggregate information from dozens of sources.

However, assurance requires more than aggregation.

It requires organisations to demonstrate:

- How information entered the system

- Who verified it

- Which controls were applied

- Whether changes were tracked

- Whether evidence was preserved

Whether management can demonstrate the state of information at the time of attestation

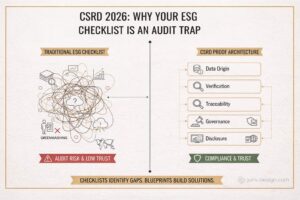

Without structured evidence architecture, organisations may possess data but lack defensible proof.

That gap often remains invisible until scrutiny occurs.

From Workflow to Control Environment

The operational implication of ISSA 5000 is straightforward.

ESG systems can no longer be viewed as reporting tools alone.

They must function as control environments.

A mature sustainability information system should be capable of demonstrating:

- Generation Controls: Information is produced through defined processes with clear ownership and documented methodologies.

- Verification Controls: Data is subject to review procedures designed to identify errors, inconsistencies and unsupported assumptions.

- Preservation Controls: Evidence is protected from unauthorised alteration and maintained in a demonstrable state.

- Governance Controls: Responsibilities, approvals and accountability mechanisms are formally established and documented.

These controls collectively form the foundation of assurance readiness.

Audit Readiness Is Not Defensibility

Many organisations believe they are prepared because they possess audit trails and documented workflows.

Those capabilities are important.

They are not sufficient.

An audit trail records activity.

Defensibility requires evidence preservation.

Audit readiness assumes cooperation.

Defensibility anticipates scrutiny.

As sustainability disclosures become increasingly relevant to investors, regulators and litigation risk, organisations must consider not only whether information can be reviewed, but whether it can be defended.

The difference is significant.

One supports reporting.

The other supports accountability.

The Governance Dimension

Perhaps the most overlooked implication of ISSA 5000 is governance.

Boards approve sustainability reports.

Management signs assertions.

These actions transform sustainability information from an operational matter into a governance matter.

The question facing leadership is therefore not:

“Can we produce the report?”

But:

“Can we demonstrate that the information was generated, verified and preserved under effective controls?”

That responsibility cannot be delegated to software.

It cannot be delegated to consultants.

Ultimately, it belongs to the organisation’s governance structure.

The Future of Assurance

The organisations that will navigate the next phase successfully are not necessarily those that disclose the most information.

They will be the organisations that understand how evidence is created, controlled and preserved.

ISSA 5000 is not simply raising expectations for sustainability reports.

It is raising expectations for sustainability systems.

And as assurance environments continue to mature, the decisive question will not be whether a report appears credible.

It will be whether the system behind it can demonstrate why it is.

Other blogs

ISSA 5000 Will Not Test Your ESG Report - It Will Test Your System

For years, sustainability reporting has been assessed primarily through the prism of...

Who Signs the ESG Report in 2027 – and Do They Understand What They Are Signing?

Most companies still see ESG as a compliance project...