CSRD and the Reality of the Balkans: Why ESG Without a System Becomes Your Biggest Hidden Risk

As 2026 approaches, CSRD (Corporate Sustainability Reporting Directive) is often perceived in the Balkans as just another administrative requirement that “comes from above.” However, when it collides with local reality, CSRD exposes a deep systemic problem: our systems were never built for provability.

Many regional companies today have ESG policies and Excel spreadsheets, but they lack what the directive actually requires a provable system that functions every day, not only at the moment the report is written.

Why Does CSRD Hit the Balkans the Hardest?

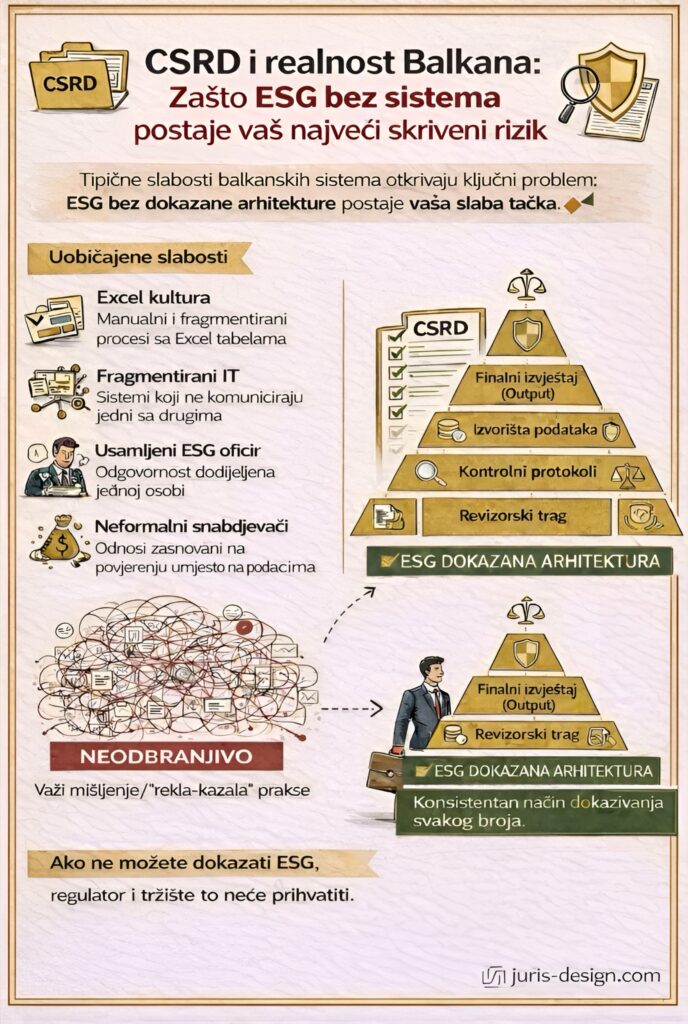

CSRD does not punish the region for being late; it exposes the fact that systems were not built on principles of traceability and auditability. Typical weaknesses that turn into risk include:

- Excel culture: Reliance on manual processes without a digital trail.

- Fragmented IT: Systems that do not communicate with each other.

- The lone ESG officer: Responsibility assigned to a single person instead of an entire governance system.

- Informal supply chains: Relationships based on trust rather than data.

ESG Without a System: How Hidden Risk Is Created

The greatest risk is not the lack of data, but the inability to prove its origin. When an auditor asks the question, “Where does this data come from and who guarantees it?”, the system often remains silent.

Without a clear proof architecture, your data is merely “he said–she said” information. If the source is unknown, the auditor cannot confirm basic accuracy, leading to the principle of “Garbage in, Garbage out.”

The Solution: ESG Proof Architecture (5 Layers of Defense)

For regional companies, the solution is not copying EU templates, but building a structure that enables traceability. Your “defense system” must consist of five key layers:

- Data Origin (Source of truth): Direct data from ERP systems, smart meters, or invoices. Without this, everything above is guesswork.

- Verification (Control point): Introducing the “four-eyes” principle — person A enters the data, person B confirms its validity.

- Traceability (Digital pedigree): A data movement map that enables reconstruction of every number back to its source.

- Governance (Accountability layer): Signed protocols and a legal framework that guarantee system integrity. If no one signs off on the data, management bears direct legal responsibility.

- Disclosure (Final window): Output in machine-readable XBRL format visible to regulators and banks.

Supply Chain: Where CSRD “Breaks”

In the Balkans, CSRD most often breaks at the supplier level. A single key partner without formal processes is enough to compromise your entire report.

In the new 2025–2026 reality, one rule applies:

A weak supplier = Your regulatory problem.

An Opportunity for Professionalization

CSRD is not just a cost; it is an opportunity to professionalize your business. Companies that build a provable system reduce long-term risk and strengthen their position in the EU market.

Remember. If you cannot prove ESG, you cannot defend it.

QUICK SELF-TEST: If an EU client asks you today:

“Can you deliver ESG data with evidence within 48 hours?”, is your answer YES — or are you at risk?

Other blogs

CSRD 2026: The Omnibus I Shift and the Standard of Due Diligence

Beyond compliance: Why evidence architecture is now a legal necessity – and a personal risk…

CSRD 2026 and Balkan

Why proof has become the new currency - and how Balkan companies can win the game...