CSRD 2026: The Omnibus I Shift and the Standard of Due Diligence

Beyond compliance: why Evidence Architecture is now a legal necessity - and a personal risk for every director who signs.

Most boards think Omnibus I bought them time. It didn’t. It transferred the risk - from the regulator to the director personally. Here is what a rigorous legal analysis of the March 2026 threshold changes actually reveals.

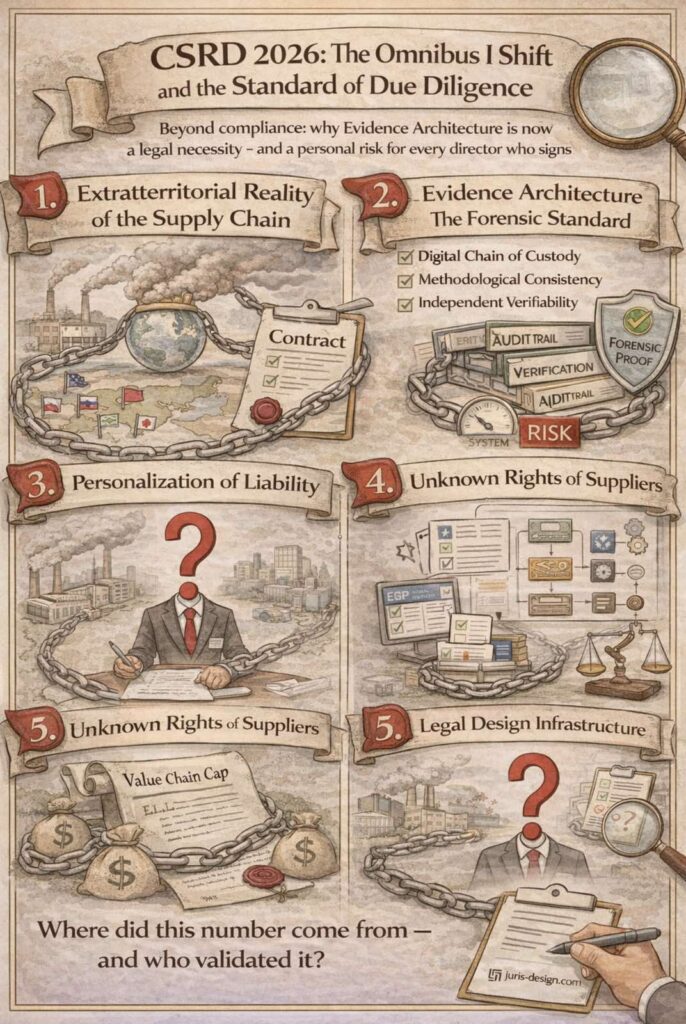

1. The Extraterritorial Reality of the Supply Chain

On March 19, 2026, the EU’s Omnibus I package raised CSRD reporting thresholds to companies with over 1,000 employees and turnover exceeding €450 million. The legislator narrowed the mandatory scope. The market did not follow.

The legal obligation to report may be bounded by thresholds. The contractual obligation to provide data is not.

If your German, Austrian, or Italian partner is CSRD-obligated -and they are - every gram of their sustainability burden travels downstream via contract. Whether you operate from Warsaw, Podgorica, Beograd, Zagreb, USA, Seoul, or São Paulo, the question has shifted permanently:

The core legal question is no longer about the mandate to report. It is about the standard of proof.

Boards that interpreted the threshold increase as a reprieve misread the signal entirely. The compliance perimeter contracted. The evidentiary expectation did not.

2. Evidence Architecture: The Forensic Standard

Sustainability data is completing a transition that began years ago: from corporate communication to legal evidence.

Across jurisdictions, a consistent pattern emerges in legal and audit practice: auditors do not challenge the data. They challenge the system that produced it.

This is what I define as Evidence Architecture - the systematic design of audit trails that can withstand not just regulatory review, but legal scrutiny. An Excel spreadsheet or a PDF without a verifiable chain of custody does not meet this standard. It is not a compliance gap. It is a liability.

What the Forensic Standard Requires:

- Digital Chain of Custody - A traceable, time-stamped record from the point of data origin to final disclosure. Not a summary. A trail.

- Methodological Consistency - Q1 data collection must be defensibly identical to Q4. Inconsistency is the first crack every auditor exploits.

- Independent Verifiability - Data that can withstand third-party assurance and, where necessary, legal scrutiny. If it cannot be verified externally, it cannot be defended internally.

3. Governance and the Personalization of Liability

This is the conversation most boards are not having - and should be.

Under the CSRD framework, sustainability reporting is elevated to board-level accountability. This is not rhetorical. It is structural. Directors who sign off on ESG disclosures that lack a robust evidentiary basis may be exposing themselves to regulatory sanctions, civil liability, and reputational consequences that follow individuals - not just organizations.

When a sustainability claim fails audit, the question shifts from what went wrong to who authorized it. In the CSRD context, that person has a name on a board resolution.

The legal framework is clear: if ESG cannot be substantiated through a designed system of proof, it represents a point of significant professional and legal exposure for those who signed it.

4. The Value-Chain Cap: A Protection Most Suppliers Don’t Know Exists

One of the most significant - and most overlooked - provisions of the Omnibus I package is the Value-Chain Cap.

This provision establishes that large EU entities cannot demand sustainability data from smaller suppliers that exceeds the voluntary SME standards arriving in July 2026. It is a genuine statutory protection. And the majority of non-EU suppliers operating in EU supply chains are entirely unaware of it.

They are overdelivering on data they are not legally obligated to provide, while underdelivering on the specific, verified data their partners actually require - creating simultaneous risks of unnecessary operational disclosure and continued liability exposure from unverified claims.

Legal Design allows us to map these boundaries clearly: to identify precisely what you must not provide, and to deliver what you do provide with forensic precision. This is not a documentation exercise. It is a rights exercise.

5. Legal Design as Operational Infrastructure

The role of the modern lawyer is not to produce more complexity. It is to make compliance possible, visible, and defensible.

Legal Design Thinking translates regulatory obligation into operational systems - visual, process-driven architectures where every data point in a sustainability disclosure has a clear, validated, auditable origin. Not hundred-page manuals that no one reads. Systems that employees can actually use and that auditors cannot dismantle.

In the CSRD era, the primary objective is not merely to report. It is to ensure that every disclosure is rooted in a designed system of truth.

Integrity Over Narrative. Regulations are subject to political and economic cycles. The structural shift toward verifiable accountability is not. The window created by Omnibus I threshold adjustments should be read precisely as that - a window, not an exit.

The organizations that will lead in this era are not those with the most elaborate sustainability narratives. They are the ones who can answer one question, instantly, from any point in their supply chain:

“Where did this number come from - and who validated it?”

The window is open. The question is whether you are building a system - or just a story.

Integrity in reporting is not found in the narrative. It is found in the evidence that supports it.

Other blogs

<a href="https://juris-design.com/eng/omnibus-shift/" title="CSRD 2026: The Omnibus I Shift and the Standard of Due Diligence“>CSRD 2026: The Omnibus I Shift and the Standard of Due Diligence

Iznad usklađenosti: zašto je Arhitektura dokaza sada pravna nužnost – i lični rizik…

CSRD 2026 and Balkan

Why proof has become the new currency - and how Balkan companies can win the game...